Risk vs. Uncertainty

A Poker analogy does not work with Trump.

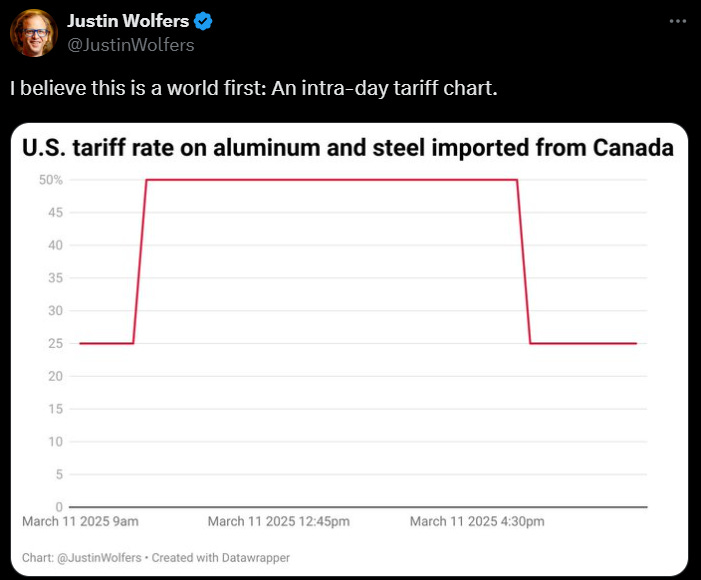

With erratic tariffs, cabinet shakeups, and mixed signals to the Fed, the President is fueling rising uncertainty in markets and the broader economy. With the specter of punishing new tariffs hanging over global trade, companies are racing to decide if they should stay abroad or rush production back to American soil. Personal spending is up, could this be because people are nervous about the future? What about the 90-day reciprocal tariff pause? What’s coming next???

When Ukrainian President Zelenskyy was at the Oval Office in February, Trump famously told him he "does not have the cards" regarding Russia's brutal invasion.

But does Trump "have the cards?" Does anyone even "have the cards"? I mean, this analogy obviously refers to gambling with cards like poker — but can we even think of the current state of the world as a game of cards?

The answer I'm obviously hinting at is: no. But why?

In economics, when we talk about probabilities, randomness, and (un)predictability, we need to make a crucial distinction between risk and uncertainty.

In this article, I will explain the concept of Knightian uncertainty and how it differs from quantifiable risk, demonstrating its significance for game theory, microeconomics, behavioral economics, and global politics.

The Difference Between Risk & Uncertainty

Economist Frank Knight (1885–1972) drew a crucial distinction between risk and uncertainty in his seminal work Risk, Uncertainty and Profit (1921):

Risk is quantifiable.

When playing roulette, both players and the casino know all possible outcomes and their exact probabilities. This measurable risk enables us to make precise calculations—like expected value—to guide decisions.

Consider a simple coin toss: If heads yields a $1,000 gain and tails results in a $1,000 loss, with a fair 50/50 coin, the expected value is exactly calculable at $0:

This implies that over an infinite number of repetitions, the game would yield zero net gain for either party - making it perfectly fair between the player and the game's proposer. Gambles with negative expected value create the house edge —ensuring the casino's long-term profitability (the house always wins).

Uncertainty is indeterminate.

Unlike measurable risk, uncertainty describes situations where neither all possible outcomes nor their probabilities are known. This absence of quantifiable parameters leaves decision-makers without reliable statistical guidance.

Imagine you’re playing a game of poker:

A standard deck has 52 cards, with 13 in each suit. By observing the cards in your hand, the community cards, and any revealed by opponents, you can estimate the likelihood of certain hands. This represents Knight’s definition of risk: probabilities derived from known variables.

Now imagine playing poker with a deck someone just Frankensteined together by mashing multiple decks together of different sizes:

How many cards are there total? Are there duplicates? Could someone get otherwise impossible hands like a five of a kind? Nobody knows!

This chaotic poker nightmare embodies pure Knightian uncertainty. Let’s visualize Knightian uncertainty in a game theoretical context.

House Party Under Uncertainty

Ava and Blake are both invited to Clara’s party next Wednesday. Ava strongly prefers attending, particularly if Blake joins, as she enjoys his company—and will go regardless of his choice. Blake, however, would only attend if Ava stays home, finding her overly talkative and draining; if she attends, he’d rather skip.

Both Ava and Blake can choose either to Go or Not Go. If we define the first element of each set as Ava’s decision and the second as Blake’s decision, Ava’s preference ordering can be described as follows:

Blake’s preference ordering is:

Here x ≻A y would mean that Ava strictly prefers x over y, same goes for Blake (≻B).

We can construct a payoff matrix based on Ava and Blake’s preferences:

Here, all numbers in red denote Ava’s payoffs while Blake’s payoffs are blue.

Ava possesses a dominant strategy: choosing Go. Regardless of Blake's decision, she always receives a higher payoff by attending the party than by abstaining.

Blake lacks a dominant strategy because his optimal choice depends entirely on Ava’s unobserved decision—a classic case of asymmetric information.

Unlike Ava, who can ignore Blake’s actions due to her dominant strategy, Blake faces Knightian uncertainty: he cannot assign meaningful probabilities to Ava’s attendance. This isn’t mere risk, but true uncertainty—the "unknown unknowns" of whether his presence will collide with Ava’s. His dilemma mirrors real-world strategic paralysis: without probabilistic anchors, rational decision-making collapses into guesswork.

Loss Aversion and Ambiguity Aversion

Let’s look at Blake’s problem through empirical findings in behavioral economics and psychology:

If I were to offer you a choice between a million dollars or a 50/50 gamble between two million or nothing, you’d probably choose the safer option of a million dollars.

However, if I reverse the question and force you to either hand over a million dollars of your own or take a 50/50 gamble between losing two million or losing nothing, you’d probably gamble and hope to keep your money.

This pattern in behavioral economic decision theory is more commonly known as loss aversion. The fact that people simply hate losing with a burning passion led psychologists like Daniel Kahneman and Amos Tversky to develop Prospect Theory, which predicts that people will act in loss-averse ways relative to a reference point of their choice.

To understand ambiguity aversion, consider Ellsberg’s Paradox with two urns:

Urn A contains 100 balls with a known distribution—50 red and 50 blue.

Urn B holds 100 balls with an unknown ratio of red to blue.

If I offer you $1,000 to pick a red ball (and replace it) from either urn, then repeat the same for blue balls, most people will pick urn A both times. However, this behavior cannot be statistically optimal:

If we prefer Urn A over Urn B when picking red balls, we’re implicitly assuming the probability of drawing red is higher from A than B. Since both urns contain 100 balls, this suggests we believe Urn B has fewer than 50 red balls. But when we repeat this preference for blue balls, we’re also implying Urn B has fewer than 50 blue balls! This is impossible—Urn B can’t simultaneously have fewer than 50 red and fewer than 50 blue balls if it holds exactly 100 balls total. The math literally doesn’t add up.

Now, if we assume that:

The probability of Ava being at the party is reasonably high, and

Blake is loss-averse or ambiguity-averse,

then the rational choice is to not attend the party.

Implications for Global Politics and Finance

Would you invest in an economy where trade policies can change instantly? Would you invest in a highly volatile startup with no backing whatsoever?

According to Nobel laureate Paul Krugman (check out his incredible Substack, if you haven’t yet), it’s not necessarily the price effects of tariffs themselves that are so destructive about Trump’s tariffs, but rather the avalanche of uncertainty created by their on-again, off-again cycles and cartoonishly large magnitude—with no predictability whatsoever.

Source: Justin Wolfers, x.com/JustinWolfers/status/1899615967354741105

Uncertainty may also explain the equity premium puzzle—the persistent gap between stocks’ high historical returns and government bonds’ meager yields. This excess return could represent the market’s risk premium for investors willing to brave unquantifiable uncertainty, not just measurable risk.

That’s the thing—if we know the possible risks, we’d be more comfortable putting our money where our mouth is. But the real world isn’t sugarcoated in known probabilities; uncertainty looms everywhere.

Fighting Uncertainty?

To mitigate uncertainty, central banks often release their plans in advance, allowing expectations and markets to adjust accordingly. This practice, known as forward guidance, enables markets to price in future rate cuts or hikes. Credible central banks combat uncertainty through trust—a reputation earned only by consistently fulfilling their promises.

Yet in today’s geopolitical arena, certainty itself has become obsolete: uncertainty now functions as the dominant strategy. This is inevitable; asymmetric information defines statecraft, for without it, secrets (and thus power) could not exist. It would be geopolitical suicide for a nation to surrender its uncertainty-fueled power, e.g. by accidentally leaking war plans over Signal, twice.

Conclusion

Ultimately, risk lacks the crippling indeterminacy of true uncertainty. Yet therein lies the strategic opportunity—by designing decision environments that exploit this asymmetry, policymakers and strategists can turn unpredictability into leverage. From social-economic games to global affairs, those who master uncertainty don't merely adapt to chaos — they weaponize it. In this high-stakes world, the ultimate power lies not in holding the cards, but in controlling the table.